Financiers have an old saying about Dominos Pizza – “it’s a data company that happens to sell pizza.” As profiled in an amazing Bloomberg feature earlier this year, the company overcame product, market, and economic struggles to build an uncompromising pizza empire that will soon have robots delivering piping-hot za’s to your front door (in New Zealand, that’s already happening).

While Dominos dominates and Shake Shack continues its ambitious expansion, the retail industry hasn’t fared as well. According to insights from S&P Global Market Intelligence, retail stores are shuttering at a concerning pace in 2017, with at least 8 household name companies like Sears knocking on bankruptcy’s door.

Amongst these distressed companies is Guitar Center, which we’ve reported on several times over the last few years. In 2007, Guitar Center was acquired in a leveraged buyout by Bain Capital (the private equity firm previously headed by Mitt Romney) for just south of $2 billion. The company has been chipping away at the debt raised for the sale, but according to a new Bloomberg report, Moody’s ratings for the remaining debt ($1.3 billion), nearly half of which is due within the next two years, could be downgraded from its already-trashy B2 Rating to junk-status.

While Guitar Center remains the dominant music instrument sales company in the U.S. – with 2013 sales of over $2 billion – they’ve been struggling to pay off this debt, in the midst of a chaotic revolving door of executives that looks basically like the plot from Silicon Valley. Nevertheless, the company continues to expand by opening up new stores, experimenting with multi-platform video content, and offering in-store lessons. Industry analyst Eric Garland argues that this expansion amounts to pre-bankruptcy preparation: mobilize finance to generate hard assets that can be sold off later.

Yves Smith of Naked Capitalism wrote yesterday that these sorts of “desperation moves” are a symptom of retail’s private equity illness:

…one of the reasons so many real world retailers are hitting the wall so hard is that private equity leverage and asset stripping made them particularly vulnerable. While the losses to online retailers would have forced some downsizing regardless, the fact that so many are making desperate moves in parallel is in large measure due to the fact that the tender ministrations of their private equity overlords have made them fragile.

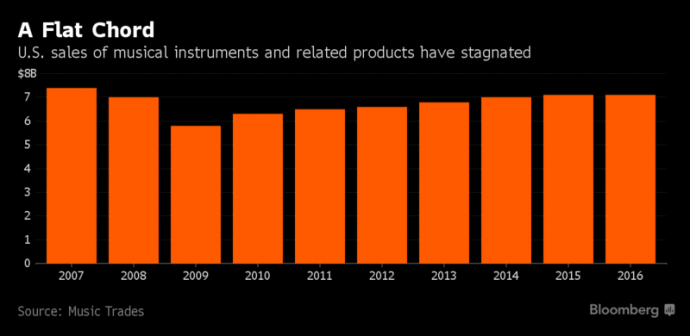

This is all happening, not incidentally, in a music instrument sales climate that’s been stagnating since 2013.

The common narrative these days is that online retail is what’s killing physical stores – in particular Amazon, whose CEO Jeff Bezos recently surpassed Warren Buffet to become the world’s second-richest man. So its interesting to see Naked Capitalism and Garland argue that the root of these sales problems may actually lie in private equity firms’ demands of companies like Guitar Center. Brian Majeski of Music Trades magazine told Bloomberg, “if you’re going to buy a $1,500 guitar, you’re not going to do it on Amazon.”

That’s a reasonable conclusion, but publications like Gear Gods have been covering the growth of specialty, niche brands like Kiesel and Vigier, neither of which drive the sales of Guitar Center, whose bread and butter remains giants like Fender and Gibson. Fender, not incidentally, is beginning to move towards direct-to-consumer sales.

All of which leaves Guitar Center in the position of Pied Piper – rushing to generate relevant products and new revenue streams while a debt-laden Sword of Damocles hangs over their head.

emetal / April 27, 2017 2:31 am

very interesting read.

/

B.C. Loy / April 27, 2017 1:42 pm

GC is a joke in the music industry.

/